3QFY2018 Result Update | Cable

February 14, 2018

Century Plyboards India

BUY

CMP

`298

Performance Update

Target Price

`400

Y/E March (` cr)

3QFY18

3QFY17

% yoy

2QFY18

% qoq

Investment Period

12 month

Net sales

510

459

11.2

475

7.5

Sector

Plywood

EBITDA

88

67

30.2

74

18.5

Market Cap (Rs cr)

6,643

EBITDA margin (%)

17.2%

14.7%

15.6%

Net Debt

545

Adjusted PAT

47

37

25.1

40

16.2

Beta

0.9

Source: Company, Angel Research

52 Week High / Low

363/213

For 3QFY2018, Century Plyboards India Ltd (CPIL) posted results in-line with our

Avg. Daily Volume

36,577

Face Value (Rs)

10

expectations on both top-line as well as bottom-line fronts. Revenues grew by

BSE Sensex

34,196

~11% yoy and operating margins were also higher yoy. On the bottom-line front,

Nifty

10,498

Reuters Code

CNTP.BO

CPIL reported growth of ~25% yoy to `47cr on the back of strong top-line growth

Bloomberg Code

CPBI.IN

and lower interest cost.

Top-line driven by healthy volume growth: The company’s top-line grew by ~11%

Shareholding Pattern (%)

yoy to `510cr on the back of healthy growth in volumes. Considering the

Promoters

72.0

segments, the company’s plywood, laminate & particle Board segment reported

MF / Banks / Indian Fls

4.7

flat growth. During the quarter, the company had started selling MDF, which

FII / NRIs / OCBs

11.5

reported ~`48cr. The logistics segment reported ~37% growth.

Indian Public / Others

11.8

Healthy revenues and lower interest cost aided overall profitability: On the

operating front, the company’s margin improved by 252bps yoy on the back of

Abs. (%)

3m

1yr

3yr

MDF contribution in total revenue, which is a higher margin business. The

Sensex

3.0

22.2

20.5

company reported ~25% yoy rise in its net profit to `47cr on the back of healthy

CPIL

6.8

41.5

60.0

revenue growth and lower interest cost.

Outlook and Valuation: We expect CPIL to report net revenue CAGR of ~17% to

~`2,896cr over FY2017-20E owing to healthy growth in plywood and lamination

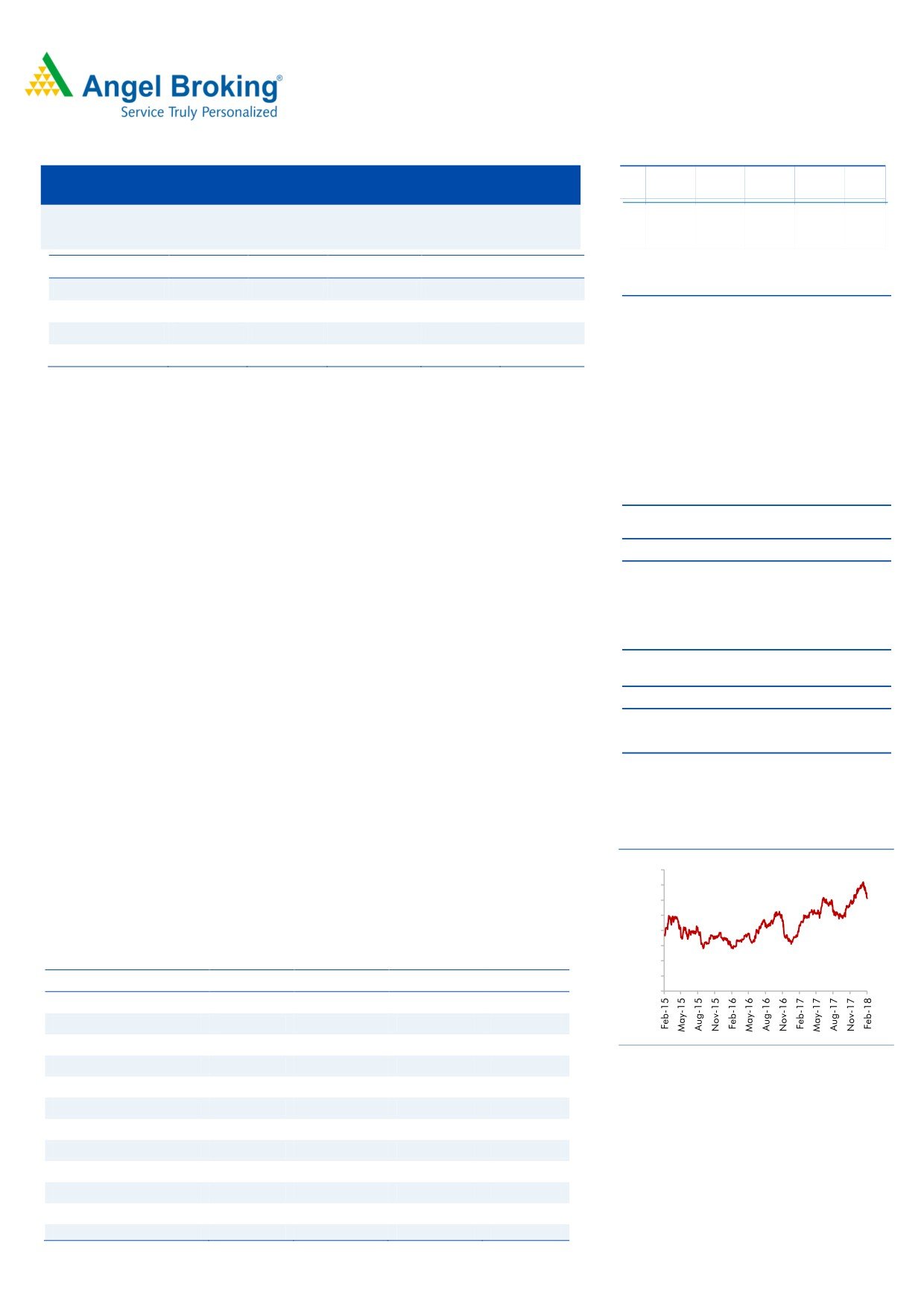

Historical share price chart

business, foray into MDF and particle boards coupled with strong brand and

400

distribution network. On the bottom-line front, we expect CAGR of ~16% to

350

300

`306cr over the same period on the back of strong revenue and better margins in

250

MDF business. We maintain our BUY rating on the stock with target price of `400.

200

150

Key Financials

100

50

Y/E March (` cr)

FY2017

FY2018E

FY2019E

FY2020E

0

Net sales

1,819

2,007

2,510

2,896

% chg

10.8

10.4

25.1

15.4

Adj. Net profit

193

188

248

306

Source: Company, Angel Research

% chg

14.0

(2.9)

31.9

23.4

EBITDA margin (%)

17.2

17.5

17.9

18.1

Amarjeet S Maurya

EPS (`)

8.7

8.4

11.1

13.7

022-40003600 Ext: 6831

P/E (x)

34.3

35.3

26.8

21.7

P/BV (x)

9.3

7.5

6.1

5.0

RoE (%)

27.1

21.3

22.9

22.9

RoCE (%)

18.9

17.1

20.2

21.3

EV/Sales (x)

3.9

3.7

2.9

2.5

EV/EBITDA (x)

23.0

21.0

16.4

13.9

Source: Company, Angel Research Note: CMP as of February 06, 2018

Please refer to important disclosures at the end of this report

1

Century Plyboards India| 3QFY2018 Result Update

Exhibit 1: 3QFY2018 Performance

Y/E March (` cr)

3QFY18

3QFY17

% yoy

2QFY18

% qoq

9MFY18

9MFY17

% chg

Net Sales

510

459

11.2

475

7.5

1,458

1,394

4.5

Consumption of RM

261

220

18.5

254

2.4

749

665

12.6

(% of Sales)

51.1

48.0

53.6

51.4

47.7

Staff Costs

72

64

13.4

68

6.9

209

190

9.9

(% of Sales)

14.2

13.9

14.2

14.3

13.6

Other Expenses

89

108

(17.1)

78

13.7

277.18

331

(16.3)

(% of Sales)

17.5

23.4

16.5

19.0

23.7

Total Expenditure

422

391

7.9

401

5.4

1,235

1,186

4.1

Operating Profit

88

67

30.2

74

18.5

223

208

7.0

OPM

17.2

14.7

15.6

15.3

14.9

Interest

6.3

11.2

(44.0)

7.9

(20.9)

20

26

(21.5)

Depreciation

26.3

14.9

76.0

13.8

90.3

53

37

44.8

Other Income

4

3

1

5

8

PBT (excl. Ext Items)

59

44

33.6

53

12.3

154

154

0.4

Ext (Income)/Expense

PBT (incl. Ext Items)

59

44

33.6

53

12.3

154

154

0.4

(% of Sales)

11.7

9.7

11.2

10.6

11.0

Provision for Taxation

13

7

13

34

24

(% of PBT)

21.5

16.1

24.2

21.7

15.7

Reported PAT

47

37

25.1

40

16.2

121

130

(6.7)

Source: Company, Angel Research

Exhibit 2: 3QFY2018 Segment Revenue Performance

Y/E March (` cr)

3QFY18

3QFY17

% yoy

2QFY18

% qoq

9MFY18

9MFY17

% chg

Plywood & allied products

322.7

323.5

(0.2)

306

5.5

971

982

(1.1)

Laminate & allied products

99.9

99.4

0.5

125

(19.9)

314

302

3.7

Medium density Fibre board

47.6

0.4

-

0

-

48

3

-

Particle Board

10.0

10.3

(2.4)

14

(30.8)

36

13

164.2

Container Frieght Station Services

27.6

20.2

36.6

25

10.3

76

65

17.7

Others

7.5

8.2

(8.1)

11

(32.0)

28

34

(18.8)

Total Segment Revenue

515

462

11.6

481.1

7.1

1473

1400

5.2

Less: Inter segment Revenue

5

3

6.6

15

5

Gross Sales

510

459

11.2

474.6

7.5

1458

1394

4.5

Source: Company, Angel Research

February 14, 2018

2

Century Plyboards India| 3QFY2018 Result Update

Outlook and Valuation

We expect CPIL to report net revenue CAGR of ~17% to ~`2,896cr over FY2017-

20E owing to healthy growth in plywood and lamination business, foray into MDF

and particle boards coupled with strong brand and distribution network. On the

bottom-line front, we expect CAGR of ~16% to `306cr over the same period on

the back of strong revenue and better margins in MDF business. We maintain our

BUY rating on the stock with target price of `400.

Downside risks to our estimates

Most of the company’s raw materials are imported from other countries,

and considering that the company has ECB loans, any unfavorable

change in currency may pose forex risks, which could significantly impact

margins.

Recently, the company has added a new MDF plant with capex of `380cr,

any slowdown in MDF market can impact the company’s earnings due

higher fixed cost overheads.

Company Background

Century Plyboards (India) Ltd (CPIL) is a plywood manufacturer. The company's

segments include plywood, laminate, CFS services and others. The company's

geographical segments are India and overseas. The plywood segment includes

plywood, block-board, veneer and timber. The laminate segment includes

decorative laminates and pre-laminated boards. The CFS services segment

includes container freight station services. The others segment includes mainly

trading of chemicals, minerals, readymade furniture and equipments. The

company's product portfolio includes doors, decorative veneer, new age products

(NAP), fiber cement boards, particle boards, look book, slimline, mono core,

magnetic laminates and prelaminated boards. CPIL is also engaged in the logistics

business through the management of a container freight station. The Company's

units are spread across India in Joka (West Bengal), Guwahati (Assam), Kandla

(Gujarat), Chennai (Tamil Nadu) and Karnal (Haryana).

February 14, 2018

3

Century Plyboards India| 3QFY2018 Result Update

Profit & Loss Statement

Y/E March (` cr)

FY2016

FY2017

FY2018E

FY2019E

FY2020E

Total operating income

1,641

1,819

2,007

2,510

2,896

% chg

3.3

10.8

10.4

25.1

15.4

Total Expenditure

1,351

1,507

1,656

2,061

2,372

Raw Material

819

895

987

1,235

1,425

Personnel

236

273

307

389

455

Others Expenses

296

339

361

437

492

EBITDA

289

312

351

449

524

% chg

7.1

7.8

12.6

27.9

16.6

(% of Net Sales)

17.6

17.2

17.5

17.9

18.1

Depreciation& Amortisation

47

59

67

75

77

EBIT

242

253

284

374

447

% chg

9.1

4.4

12.6

31.6

19.5

(% of Net Sales)

14.7

13.9

14.2

14.9

15.4

Interest & other Charges

48

30

55

70

70

Other Income

6

23

8

9

10

(% of PBT)

3.0

9.2

3.4

2.9

2.6

Share in profit of Associates

-

-

-

-

-

Recurring PBT

200

245

238

314

387

% chg

11.5

22.4

(2.9)

31.9

23.4

Tax

30

52

50

66

81

(% of PBT)

15.2

21.0

21.0

21.0

21.0

PAT (reported)

170

193

188

248

306

Minority Interest (after tax)

-

-

-

-

-

Profit/Loss of Associate Company

-

-

-

-

-

ADJ. PAT

170

193

188

248

306

% chg

13.9

14.0

(2.9)

31.9

23.4

(% of Net Sales)

10.3

10.6

9.4

9.9

10.6

Basic EPS (`)

7.6

8.7

8.4

11.1

13.7

Fully Diluted EPS (`)

7.6

8.7

8.4

11.1

13.7

% chg

13.9

14.0

(2.9)

31.9

23.4

February 14, 2018

4

Century Plyboards India| 3QFY2018 Result Update

Balance Sheet

Y/E March (` cr)

FY2016

FY2017

FY2018E FY2019E FY2020E

SOURCES OF FUNDS

Equity Share Capital

22

22

22

22

22

Reserves& Surplus

507

693

858

1,062

1,312

Shareholders Funds

529

715

881

1,084

1,334

Minority Interest

9

12

12

12

12

Total Loans

474

619

780

770

770

Deferred Tax Liability

1

1

1

1

1

Total Liabilities

1,013

1,347

1,674

1,867

2,118

APPLICATION OF FUNDS

Gross Block

298

412

924

948

973

Less: Acc. Depreciation

48

106

173

248

325

Net Block

250

306

751

700

648

Capital Work-in-Progress

102

299

299

299

299

Investments

6

6

6

6

6

Current Assets

751

905

836

1,139

1,480

Inventories

298

301

330

426

500

Sundry Debtors

284

342

379

488

571

Cash

39

67

34

46

96

Loans & Advances

90

160

60

138

261

Other Assets

39

35

32

40

52

Current liabilities

162

238

286

345

385

Net Current Assets

588

667

549

793

1,095

Deferred Tax Asset

66

69

69

69

69

Mis. Exp. not written off

-

-

-

-

-

Total Assets

1,013

1,347

1,674

1,867

2,118

February 14, 2018

5

Century Plyboards India| 3QFY2018 Result Update

Consolidated Cashflow Statement

Y/E March (` cr)

FY2016

FY2017

FY2018E FY2019E FY2020E

Profit before tax

200

245

238

314

387

Depreciation

47

59

67

75

77

Change in Working Capital

34

(54)

84

(232)

(251)

Interest / Dividend (Net)

47

30

55

70

70

Direct taxes paid

(47)

(43)

(50)

(66)

(81)

Others

10

(17)

0

0

0

Cash Flow from Operations

293

221

394

160

202

(Inc.)/ Dec. in Fixed Assets

(150)

(305)

(512)

(24)

(25)

(Inc.)/ Dec. in Investments

11

0

0

0

0

Cash Flow from Investing

(139)

(304)

(512)

(24)

(25)

Issue of Equity

0

0

0

0

0

Inc./(Dec.) in loans

(44)

142

162

(10)

0

Dividend Paid (Incl. Tax)

(50)

(0)

(22)

(45)

(56)

Interest / Dividend (Net)

(59)

(30)

(55)

(70)

(70)

Cash Flow from Financing

(153)

112

85

(124)

(126)

Inc./(Dec.) in Cash

1

28

(33)

12

51

Opening Cash balances

37

39

67

34

46

Closing Cash balances

39

67

34

46

96

February 14, 2018

6

Century Plyboards India| 3QFY2018 Result Update

Key Ratios

Y/E March

FY2016

FY2017

FY2018E FY2019E FY2020E

Valuation Ratio (x)

P/E (on FDEPS)

39.1

34.3

35.3

26.8

21.7

P/CEPS

30.5

26.2

26.0

20.5

17.3

P/BV

12.5

9.3

7.5

6.1

5.0

Dividend yield (%)

0.8

0.8

0.3

0.7

0.8

EV/Sales

4.3

3.9

3.7

2.9

2.5

EV/EBITDA

24.4

23.0

21.0

16.4

13.9

EV / Total Assets

7.0

5.3

4.4

3.9

3.4

Per Share Data (Rs)

EPS (Basic)

7.6

8.7

8.4

11.1

13.7

EPS (fully diluted)

7.6

8.7

8.4

11.1

13.7

Cash EPS

9.8

11.4

11.4

14.5

17.2

DPS

2.2

2.5

1.0

2.0

2.5

Book Value

23.8

32.1

39.6

48.7

60.0

Returns (%)

ROCE

24.1

18.9

17.1

20.2

21.3

Angel ROIC (Pre-tax)

25.3

20.0

17.6

20.8

22.3

ROE

32.1

27.1

21.3

22.9

22.9

Turnover ratios (x)

Asset Turnover (Gross Block)

5.5

4.4

2.2

2.6

3.0

Inventory / Sales (days)

66

60

60

62

63

Receivables (days)

63

69

69

71

72

Payables (days)

19

28

31

31

31

Working capital cycle (ex-cash) (days)

110

101

98

102

104

Source: Company, Angel Research

February 14, 2018

7

Century Plyboards India| 3QFY2018 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Angel Broking Pvt. Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavours to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Pvt. Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking

or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or

in the past.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Century Plyboards India

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to -15%)

Sell (< -15%)

February 14, 2018

8